If you’re an owner-manager on salary in your CCPC and you always get a big RRSP refund, you may be able to improve monthly cash flow by reducing tax withheld at source using CRA Form T1213. Here’s how it works, who qualifies, what CRA requires, and how to avoid surprises at tax time.

Why owner-managers get big RRSP refunds on salary

If you’re an owner-manager of a CCPC (a Canadian-controlled private corporation) and you pay yourself a salary, your corporation must run payroll like any other employer. That means income tax is withheld from each paycheque based on payroll tables - not based on what you plan to deduct later on your personal return.

If you then maximize your RRSP (Registered Retirement Savings Plan) using personal contributions you make yourself, your RRSP deduction reduces your taxable income when you file your T1 return.

Result: you often get a large refund, because too much tax was withheld during the year.

That refund feels nice - but it usually means you gave the CRA an interest-free loan all year.

What we’ll cover:

Why payroll withholding doesn’t “know” about your RRSP plan

How Form T1213 can reduce tax withheld each pay period

CRA conditions you must meet before applying

RRSP-specific details CRA looks for

How to apply (and where to submit)

Common mistakes and how to avoid a balance owing

A simple cash-flow comparison and FAQs

The “better way”: reduce tax withheld using Form T1213

CRA allows employees (including owner-managers on payroll) to request reduced tax deductions at source when they have deductions or credits that payroll doesn’t account for.

The most common example for incorporated business owners: deductible RRSP contributions you make personally during the year.

CRA’s payroll guidance is clear: to reduce income tax withheld at source in these situations, you generally need a CRA “letter of authority” - and one way to request it is Form T1213.

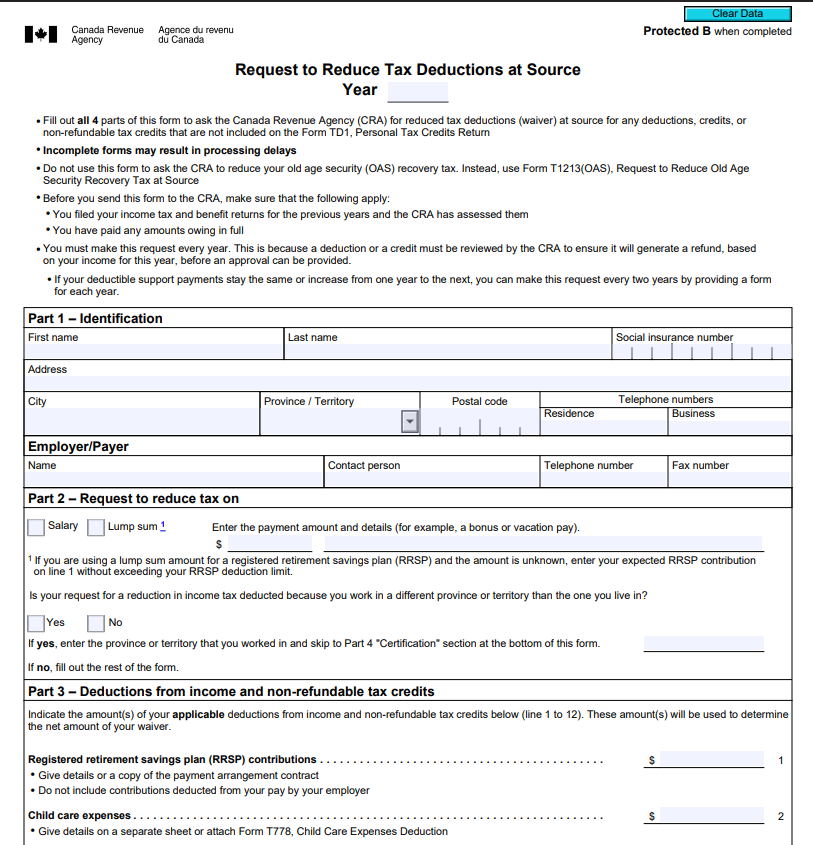

Form T1213

What Form T1213 does (and what it doesn’t)

Form T1213 (“Request to Reduce Tax Deductions at Source”) is how you ask CRA to approve lower tax withholding because you expect specific deductions/credits that aren’t part of your TD1.

What it does:

Can increase monthly cash flow by reducing tax withheld from each paycheque (after CRA approves and issues a letter).

What it doesn’t:

It does not change your actual tax liability - only when you pay it.

It does not let you and your corporation “just decide” to withhold less without CRA approval (CRA’s payroll rules explicitly require the letter of authority).

TD1 vs T1213 (quick difference)

TD1 forms are where you claim standard personal credits that payroll can apply directly.

T1213 is for other deductions/credits not included on TD1, such as RRSP contributions you make yourself, charitable donations, child care expenses, etc.

Who should consider T1213 in a CCPC

T1213 is worth considering if you are:

On salary from your CCPC (regular payroll), and

You consistently contribute to your personal RRSP during the year, and

You reliably receive a large refund mainly because of those RRSP deductions.

It can also be useful if you have other predictable deductions/credits CRA lists (donations, certain employment expenses, child care expenses, etc.).

CRA’s rules you must meet before you apply

CRA includes some practical “gatekeeping” rules right on the T1213 form. Before you submit, make sure these are true:

You’ve filed your income tax and benefit returns for previous years and CRA has assessed them.

You’ve paid any amounts owing in full.

You generally must apply every year, because CRA reviews whether the request is expected to generate a refund based on your income and deductions for that year.

(There’s a limited note on the form about support payments potentially being requested every two years if they stay the same or increase, but most owner-manager RRSP situations should assume annual requests.)

RRSP-specific tips that matter for T1213 approval

Payroll RRSP vs personal RRSP (important distinction)

CRA’s T1213 form is explicit for the RRSP line item:

You can request a reduction for RRSP contributions, but you must not include contributions deducted from your pay by your employer.

In plain English:

If your corporation runs a setup where RRSP contributions are taken off your pay (like a group RRSP style arrangement), the payroll withholding may already reflect that structure.

If you contribute personally from your bank account, payroll withholding usually won’t reflect it - this is where T1213 is commonly used.

Don’t exceed your RRSP deduction limit

Your RRSP deduction limit (your “room”) controls how much you can deduct. CRA tells you where to find it:

In your CRA account, or

On the RRSP Deduction Limit Statement on your latest Notice of Assessment / Reassessment.

If you contribute more than allowed, you can run into RRSP excess contribution issues (CRA notes a 1% per month tax may apply when unused contributions exceed the limit by more than $2,000).

Know the RRSP deadline for the current tax year

For the 2025 tax year, CRA lists:

March 2, 2026 as the RRSP/PRPP/SPP contribution deadline for claiming a deduction on your 2025 return.

(Deadlines change each year based on the calendar, so always check CRA’s “Important dates” page for the applicable year.)

How to apply: step-by-step (including where to send it)

Here’s the practical workflow most owner-managers follow:

Estimate your annual RRSP contributions Use realistic numbers you can stick to (monthly or per-pay contribution plan).

Gather CRA’s supporting documents For RRSP contributions, the form asks you to give details or a copy of the payment arrangement contract (and again, don’t include employer-deducted contributions). Tip: CRA generally wants evidence this is a real, ongoing plan - not a wish.

Complete all parts of Form T1213 CRA warns incomplete forms can cause delays.

Submit to CRA (online is often easiest) CRA’s T1213 instructions say you can submit:

Online through My Account (or Represent a Client) using “Submit documents,” selecting the topic “Contact Centre and International Correspondence,” or

By mail or fax to the Sudbury Tax Centre (address and fax numbers are listed on the form).

Wait for CRA’s letter of authority CRA’s payroll guidance: the employee must obtain the letter of authority first.

What happens after CRA approves it

Once you get the CRA letter of authority, you give it to your corporation’s payroll administrator.

CRA tells employers what to do next:

Keep the letter with the employee’s records (don’t send a copy back to CRA), and

Reduce income tax withheld by the amount specified in the letter.

Common mistakes that cause delays (or create a tax bill)

Applying without being up to date If prior-year filings aren’t assessed or you have an unpaid balance, CRA says you should not send the form until those conditions are met.

No proof you’ll actually contribute For RRSP requests, CRA asks for details / a payment arrangement contract.

Reducing withholding without the CRA letter CRA’s payroll guidance requires the letter of authority before the employer reduces income tax deductions at source.

Over-reducing and ending up owing at tax time If your RRSP contributions don’t happen as planned, you can create a personal tax balance owing (and possibly instalment issues depending on your situation).

A simple cash-flow comparison

Below is a simple way to think about it: same total tax, different timing.

You are not “saving more tax” with T1213 - you’re aligning payroll withholding with deductions you’re already planning to claim.

Table 1: Refund vs. higher monthly cash flow (conceptual)

Approach

What happens during the year

What happens at tax filing

Cash-flow feel

No T1213 Wait for refund

Payroll withholds tax as if you won’t claim your personal RRSP deduction.

RRSP deduction reduces taxable income → large refund.

Lower monthly cash flow, bigger “lump sum” later.

With T1213 Reduce withholding

After CRA approval, payroll withholds less tax based on the authorized reduction.

Refund is smaller (because you already received the benefit through payroll).

Higher monthly cash flow, smaller refund later.

Note: T1213 reduces withholding timing. It does not change your RRSP deduction rules or your final tax outcome.

FAQs

1) Can an owner-manager in a CCPC use Form T1213?

Yes. If you’re on salary payroll (an employee of your corporation), you can apply like any other employee. CRA’s process is employee-driven: you request a letter of authority, then payroll can reduce withholding once you provide the letter.

2) Can my corporation just withhold less because I own the company?

Not properly. CRA’s payroll guidance requires a letter of authority to reduce income tax withheld in the situations listed (including deductible RRSP contributions you make yourself).

3) Do I need to apply every year?

Generally, yes - CRA states you must make the request every year because the deduction/credit must be reviewed for that year before approval is provided.

4) What does CRA want as proof for RRSP contributions?

T1213 specifically asks you to give details or a copy of the payment arrangement contract for RRSP contributions.

5) Can I include RRSP contributions that come off my paycheque?

CRA says do not include contributions deducted from your pay by your employer on the RRSP line of T1213.

6) Where do I submit Form T1213?

CRA’s form instructions allow submission:

Online through My Account / Represent a Client (“Submit documents”), or

By mail/fax to the Sudbury Tax Centre (details are on the form).

7) How do I find my RRSP deduction limit?

CRA says you can find it in your CRA account or on your latest Notice of Assessment / Reassessment.

8) What’s the RRSP deadline for the 2025 tax year?

CRA lists March 2, 2026 as the deadline to contribute for the 2025 tax year.

Final takeaway (and how Coral CPA can help)

If you’re an owner-manager on salary and you reliably maximize your personal RRSP every year, Form T1213 can be a smart cash-flow move: you may be able to reduce tax withheld on each paycheque (after CRA approval) instead of waiting for a large refund.

The key is doing it cleanly: make sure you’re up to date with CRA, stay within your RRSP room, provide the right support, and implement the CRA letter exactly in payroll.

If you want help setting the right salary level, structuring RRSP contributions, and preparing a strong T1213 package (so your payroll and personal tax plan actually match), Coral CPA can help you build a simple, compliant owner-manager cash-flow strategy.